Why Do Solana Apps Keep Winning?

Apps Are Winning on Solana

TL;DR

- Solana's App RCR reached 262.8% in Q3 2025, meaning applications earned $584M while the network earned $222M, apps captured 2.6x more than the protocol, nearly doubling from 132.5% in Q1 2025.

- Solana maintained 19 consecutive months of dApp revenue leadership (April 2024-November 2025), peaking at 72% global market share in January 2025 with $650M+ monthly revenue, settling at $100M and 31% global share by November 2025.

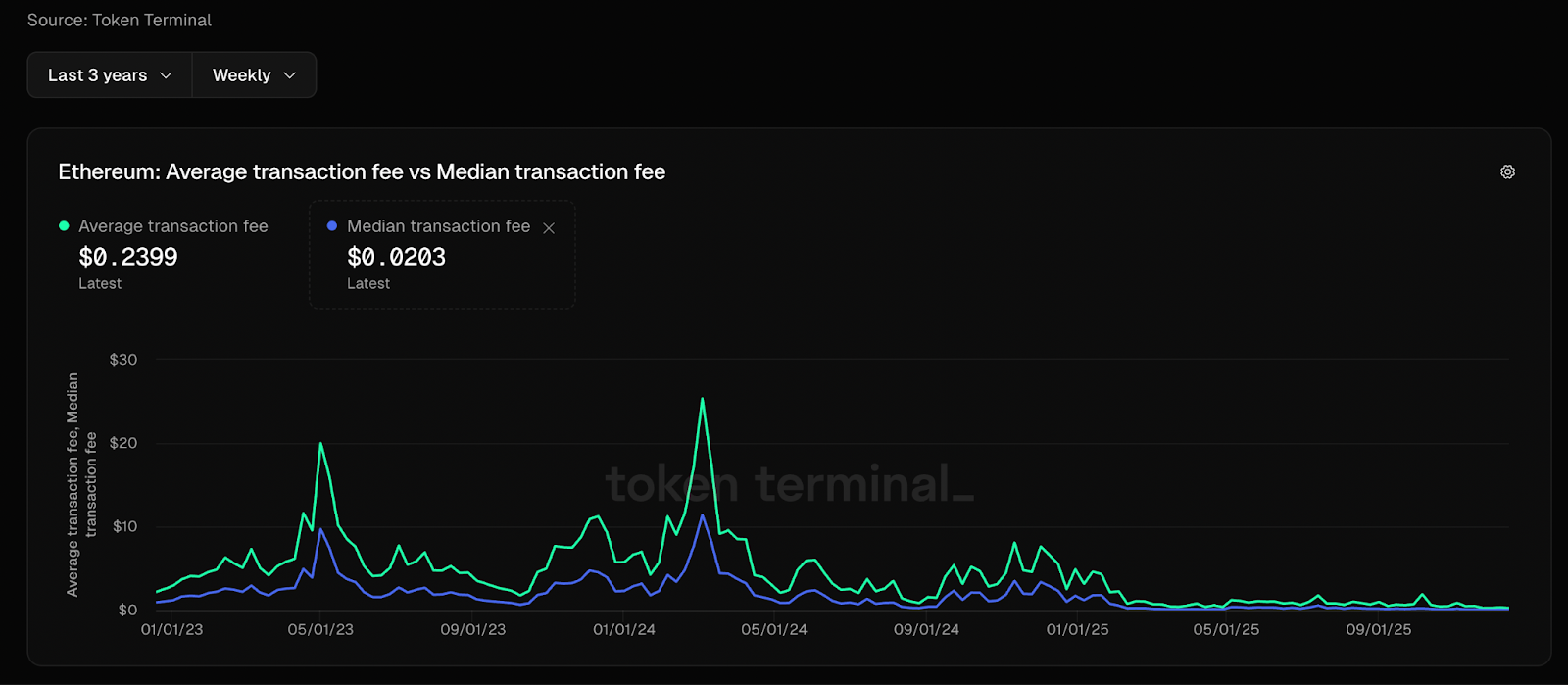

- Ultra-low transaction costs enable apps to charge meaningful fees without pricing out users, 50-100x lower than Ethereum's $0.05-$0.15 median.

- Prop AMMs demonstrate the model at maximum efficiency: capturing 60% of SOL/USDC trading volume while generating 20% of all Solana transactions but paying only 2% of network fees, market makers update prices 175x/second for ~$15/hour in costs while processing $1B+ daily volume.

- The top 8 apps captured 78% of November 2025 revenue, with individual earnings between $2.2M and $33M.

In the traditional Web2 app economy, there's a clear division: platforms (like iOS or Android) provide the underlying infrastructure and distribution channels, while applications deliver the actual user experiences, streaming, ride-hailing, marketplaces, and capture the lion's share of revenue and value. Even though app stores take a cut, the vast majority of economic upside flows to the app layer, enabling trillion-dollar companies.

This is the "Fat App" model: applications, not platforms, dominate value capture.

But here's the key question for web3 builders today: In Web2, apps routinely scale to billion-dollar (or trillion-dollar) businesses. If you're building an app on a blockchain like Solana, are you just funnelling users and fees upward to enrich the protocol... or can you actually capture meaningful value and build a sustainable, high-scale business yourself?

Solana provides the clearest real-world proof that the "Fat App" model can thrive in crypto.

Solana's App Revenue Dominance

In April 2024, Solana became the chain with the most revenue-generating applications, a position it has held for 19 consecutive months through November 2025.

Solana peaked at around 72% global market share in January 2025, fueled by explosive memecoin trading around launches like TRUMP and MELANIA (the TRUMP token launched on January 17, 2025), which drove monthly dApp revenue to record highs exceeding $650 million.

Even as competition intensified and the memecoin frenzy cooled, Solana maintained strong performance. In November 2025, Solana generated $100M in dApp revenue and accounted for 31% of the global total.

Source: Syndica

The metric that proves it: App Revenue Capture Ratio (App RCR)

There is a simple way to measure whether builders are feeding the blockchain or capturing real value: compare how much applications earn versus how much the network earns. This metric is called the Application Revenue Capture Ratio, or App RCR.

The formula is straightforward:

App RCR = Application Revenue ÷ Network Revenue (REV)

Application Revenue is everything apps earn from users: trading fees, platform fees, service charges, all the ways apps monetize beyond just processing transactions.

Network Revenue (REV) is everything paid to validators: base transaction fees, priority fees, and MEV tips.

How to interpret App RCR:

- Below 100%: The blockchain captures more value than applications. Apps are essentially subsidizing the network.

- Above 100%: Applications capture more value than the network. This is the Fat App model working. Builders win.

A higher App RCR signals a mature ecosystem where applications effectively monetize activity. A low App RCR may indicate untapped potential for developers or a nascent ecosystem not yet ready for monetization.

Solana vs Ethereum: Where Apps Win More

Both chains show the Fat App model working, but Solana's numbers reveal a more mature app economy where builders capture significantly more value.

Q1 2025: Solana Apps Already Ahead

Solana: 132.5%

- Applications earned: $1.08 billion

- Network earned: $816 million

- Apps captured 1.3x what the network did

Ethereum: 65.3%

- Applications earned: $184 million

- Network earned: $282 million

- Apps captured only 0.65x what the network did—the network dominated

Q2 2025: The Gap Widens

Solana: 222.8% (+68% QoQ)

- Applications earned: $607 million

- Network earned: $272 million

- Apps captured 2.2x what the network did

Ethereum: 107.1% (+64% QoQ)

- Applications earned: $138 million

- Network earned: $129 million

- Apps captured 1.07x what the network did—just crossed breakeven

Q3 2025: Solana Apps Dominate

Solana: 262.8% (+18% QoQ)

- Applications earned: $584 million

- Network earned: $222 million

- Apps captured 2.6x what the network did

Ethereum: 179.5% (+68% QoQ)

- Applications earned: $257 million

- Network earned: $143 million

- Apps captured 1.8x what the network did

Solana Source: Messari Solana state report

Ethereum Source: DefiLlama (App Revenue) and Blockworks Research (Network REV)

By Q3 2025, Solana apps capture 46% more value relative to the network than Ethereum apps (262.8% vs 179.5%). In Q1 2025, Solana apps earned 1.3x what the network did. By Q3 2025, that ratio doubled to 2.6x. Over three quarters, App RCR increased 98%, nearly doubling from 132.5% to 262.8%.

What this means in practice

An App RCR above 100% means applications charge their own fees on top of network costs. When someone trades on a DEX, they pay two separate fees:

Payment 1: To Solana $0.0007 (network fee to validators)

Payment 2: To the application 0.25% of trade value (application fee)

On a $10,000 trade:

- Solana earns: $0.0007

- Application earns: $25

The application captures 35,000x more than the network on that single transaction. Multiply this across billions in volume and you see how applications generate eight and nine-figure quarterly revenue while network costs stay negligible.

Transaction Fees: The Economics Behind App Profitability

The 262.8% App RCR in Q3 2025 exists because of fundamental transaction fee economics on Solana.

Every user interaction (swaps, mints, trades) incurs a tiny network fee, but when those fees stay ultra-low for the majority of users, apps can layer competitive monetization on top without pricing out users or eroding margins.

Two metrics matter: average fees and median fees. Understanding both reveals whether you can build a sustainable business.

- Average fee: Total fees divided by transactions. This gets skewed upward by a small fraction of "premium" transactions

- Median fee: The middle value when sorted. This reflects what the typical user actually pays for standard interactions.

Over the past three years (2023–2025), Solana's median fee has remained remarkably stable even as activity exploded. As of December 2025, the median sits at ~$0.0005–$0.001 (less than a tenth of a penny), while averages range $0.002–$0.01, a 3–10x gap.

Stress test: The TRUMP token launch (mid-January 2025) was Solana's most extreme congestion event ever. Daily network revenue hit records as trading volume surged. Yet even during peak chaos:

- Average fee spiked to $0.03+

- Median fee rose modestly to ~$0.001–$0.003 (barely 2–4x normal)

A core reason for this stability is Solana's local fee market design. Unlike traditional global fee markets (where congestion anywhere raises costs everywhere), Solana aims to isolate fee pressure to specific "hotspots", particular accounts or programs experiencing intense demand (e.g., a viral memecoin launch). In theory, this allows unrelated activity (simple transfers or other dApps) to proceed at baseline costs, even during network-wide peaks.

Contrast with Ethereum: Global Fee Markets

Ethereum operates a global fee market where all transactions compete for blockspace. When demand spikes anywhere, fees rise for everyone.

Current Ethereum L1 fees (December 2025):

- Average: $0.20–$0.50

- Median: $0.05–$0.15

- Solana's median is 50–100x lower

During congestion (historical peaks):

- March 2024: Average ~$25, Median ~$11

- May 2023: Average ~$20, Median ~$10

On Ethereum, high demand forces typical users to pay dramatically more or migrate to Layer 2s, fragmenting liquidity.

In short: On Solana today, you're not just feeding the blockchain. Low, predictable network costs empower successful apps to fatten up, capturing sustainable, Web2-scale revenue. The "Fat Protocol" inversion dominated early crypto, but on high-performance chains like Solana, the "Fat App" era has firmly arrived. Builders win.

Who's Winning: Top Revenue-Generating Applications

Of the 56 Solana dApps tracked in November 2025, the top 8 captured 78% of the revenue, ranging from $2.2M to $33M each.

The driver is simple: trading. Users flock to advanced terminals and wallets for fast execution, spot and perpetual exchanges, memecoin launchpads, and tools for reliable transactions. These bring liquidity, assets, and developers, who expand into new areas like tokenized real-world products.

Raydium: $154.3M

Raydium monetizes Solana’s trading volume by charging fees on every swap executed through its liquidity pools. Every swap executed on Raydium incurs a trading fee, 25 basis points on standard AMM pools, and between 1 and 100 basis points on CLMM and CPMM pools, depending on the pool design.

Fees are used to buy back RAY tokens, linking on-chain activity to application-level value capture. Applications like Raydium do not merely benefit from cheap blockspace, they transform high-frequency user activity into sustained revenue streams, reinforcing why trading-focused applications dominate Solana’s revenue rankings.

Pump.fun: $850.0 M

Pump.fun remained Solana's most profitable dApp in November 2025, capturing 90% of memecoin launchpad revenue despite the broader memecoin slowdown. The platform acquired Padre and rebranded it as Terminal, a multichain trading terminal. November 2025 was Terminal's first full month, generating $1.6M in revenue.

The memecoin launchpad sector reached a new 12-month low in November 2025, with total sector revenue declining to $36M. However, Pump.fun continued to dominate. In September 2025, the platform introduced Project Ascend, a rewards mechanism with dynamic, tiered fees tied to market cap, leading to 17,000 new streamers onboarding in the weeks following launch.

Jupiter: ~$139.94M

Jupiter's November 2025 revenue of ~$10.3M represents a lower bound, as it excludes Jupiter Lend, Studio, and Prediction Markets. Revenue came from perpetuals (largest contributor), Ultra Swaps, DCA, and limit orders.

Product diversification enhances resilience throughout market cycles. In Q3 2025, Jupiter's TVL increased 59.6% quarter-over-quarter to $2.6 billion, reclaiming second place in Solana DeFi TVL with a 22.1% market share.

Jupiter Lend, powered by Fluid and announced at Accelerate 2025 in May, launched in August 2025 and had $702.7 million in TVL by the end of Q3 2025. In September 2025, Jupiter announced its prediction market product, powered by Kalshi's liquidity.

The protocol is adding jupUSD (a native stablecoin in partnership with Ethena) and JupNet (an interchain liquidity product).

A special category worth highlighting is proprietary AMMs (or Prop AMMs), professional market makers like HumidiFi, SolFi (from Ellipsis Labs), and Tessera (Wintermute).

Prop AMMs: High-Frequency Revenue at Scale

Proprietary AMMs (Prop AMMs) prove Solana's cost structure enables entirely new market designs that are impossible on expensive chains.

What makes them different: Traditional AMMs like Raydium or Orca are passive, they set prices based on a formula and wait for trades to move the market. Prop AMMs are; they continuously update prices based on real-time market data from centralized exchanges, adjusting quotes multiple times per second without needing any trades to happen. Think of them as professional trading firms that moved their execution logic directly onchain instead of running it on private servers.

The breakthrough: Updating prices costs almost nothing on Solana. HumidiFi optimized its price updates to just 143 compute units, costing $0.0018 per update. A typical swap through Jupiter costs 150,000 compute units, over 1,000x more.

The numbers:

Prop AMMs now dominate Solana's spot markets:

- 60% of SOL/USDC trading volume flows through Prop AMMs

- $1+ billion in daily volume across all Prop AMMs consistently

- 20% of all Solana transactions are Prop AMM price updates

- Only 2% of total network fees

That ratio, 20% of transactions but only 2% of costs, proves the model works. On expensive chains, this is impossible. The fees would exceed profits from spreads.

The revenue model: Major operators include SolFi (run by Ellipsis Labs), HumidiFi, Tessera (operated by Wintermute), and ZeroFi. They earn from spreads, buying slightly below market and selling slightly above. At $1 billion+ daily volume, even single-basis-point spreads generate substantial income while network costs stay under $100 per day.

Market makers update prices 175 times per second. At $0.0018 per update, that equals approximately $15 per hour while processing millions in trading volume. On expensive chains, this frequency would cost thousands daily.

Why this only works on Solana: Low-cost updates are the foundation. Jupiter aggregator dominance provides distribution, over 40% of Solana's DEX volume flows through aggregators, with Jupiter capturing 86%. Prop AMMs integrate once with Jupiter and instantly access massive retail flow.

Right now, about 30-50 crypto pairs have active Prop AMM markets. The model scales to any liquid asset: tokenized stocks, bonds, commodities, real-world assets. When that expands to thousands of assets, those 175 updates per second multiply across every market. This infrastructure demonstrates how applications can scale revenue dramatically while maintaining minimal blockchain expenses, proving the Fat App model at scale.