MEV: What Is It And Why Should You Care? (Part 1)

On March 12, 2026, a user on Aave's interface tried to swap $50.4 million worth of USDT into AAVE tokens. Before confirming, the interface showed them the quote: $50 million in exchange for fewer than 140 AAVE. The price impact was 99%. There was a checkbox warning about this. They confirmed anyway.

Within seconds, $50 million was gone. They received 324 AAVE tokens worth about $36,000.

The money didn't disappear. Here's where it went:

- ~$10–12.5 million to MEV bots that jumped ahead of the trade and sold into it

- ~$34 million to Titan, a block builder that controlled transaction ordering

- ~$2–3.5 million to liquidity providers and arbitrage bots

- ~$600K in protocol fees, which Aave later refunded

None of these actors did anything illegal. The infrastructure to exploit the trade was already running. When a large trade creates a significant price imbalance, the bots and solvers already running will capture whatever value that imbalance produces.

That infrastructure is MEV.

This is the first part of a series on MEV on Solana. We start with the fundamentals: what MEV is, who the actors are, and how Solana's architecture shapes the way it plays out. Each part will go deeper: into the data, the infrastructure, the economics, and the ongoing arms race between those extracting value and those trying to stop it. If you're new to MEV, start here. If you're not, this will fill in the gaps.

What is MEV?

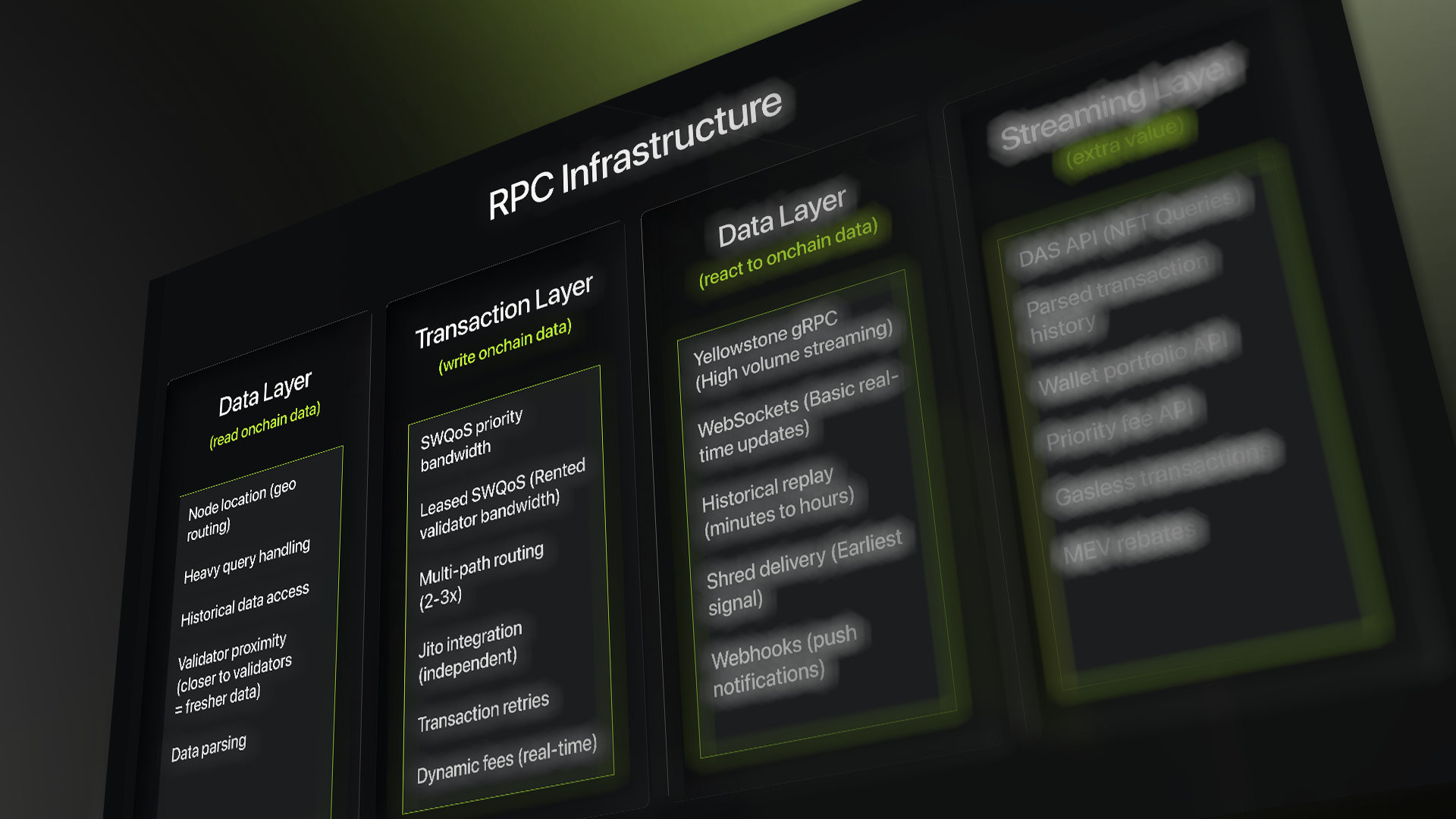

MEV, or Maximal Extractable Value, is the profit that can be extracted by manipulating transaction sequencing within a block: adding, removing, or reordering transactions before they're finalized on-chain. The value can be captured at different layers, by validators who control block production, by searchers running bots, or by the applications and protocols users trade through.

Validators (Block Producers) sit at the top. They're assigned slots to produce blocks and have complete authority over what transactions go in and in what order. That power makes them the ultimate gatekeepers of every MEV opportunity on the network.

Some validators have taken this further, multiple operators on Solana have reported receiving detailed proposals from private mempool operators, offering profit shares in exchange for transaction flow access. In June 2024, the Solana Foundation pulled 32 validators from its delegation program for running sandwich infrastructure.

~~

Searchers are the hunters, sophisticated bots that scan the network continuously looking for profitable ordering opportunities. When they find one, they simulate it, calculate what it's worth, and submit a bundle with a tip sized precisely to outbid competitors. These bundles are atomic, meaning all-or-nothing, if any transaction in the bundle fails, the whole thing reverts, so searchers only pay when they win.

Speed and infrastructure are everything here, especially on Solana where there's no public mempool to peek at. Searchers often need to run their own nodes or co-locate with high-staked validators just to get a fast enough view of the chain state to compete.

~~

Infrastructure providers like Jito are the plumbing connecting searchers and validators. Jito is the dominant MEV infrastructure on Solana, a modified validator client run by over 92% of validators by stake that adds an off-chain auction layer on top of Solana's native block production.

They run the auction systems that let searchers bid for precise transaction positioning, take a small fee on every tip, and effectively set the rules of the game for everyone operating on top of them. Importantly, Jito isn't just an MEV tool anymore, many applications use Jito bundles simply for fast, reliable transaction inclusion, bypassing priority fees entirely.

~~

How Solana's MEV differs from Ethereum

That Aave trade happened on Ethereum, where block builders like Titan could see the transaction in a public mempool, reorder it, and extract millions. On Solana, the architecture is fundamentally different.

Ethereum has a public mempool where every pending transaction is visible. Specialized builders construct entire blocks off-chain and validators simply pick the highest-paying one. Solana has neither. Transactions route directly to the current block leader, blocks are produced continuously within ~400ms slots, and validators build their own blocks.

This shapes which MEV is easy to pull off. Arbitrage, liquidations, and back-running react to confirmed state, no mempool needed. Front-running and sandwiching require seeing a transaction before it lands. Without a public mempool, that surface area is smaller on Solana, but it doesn't disappear. Validators see every incoming transaction, and that visibility can be rebuilt through out-of-protocol mempools.

The net result: Solana MEV is less about watching a public queue and more about who has the fastest infrastructure and access to transaction flow.

The forms of MEV on Solana

1. Arbitrage

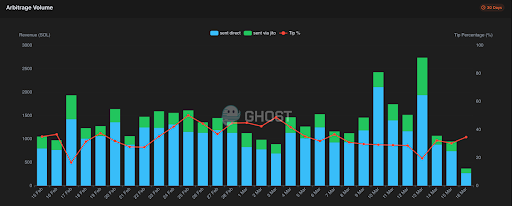

When the same asset trades at different prices across two venues, an arbitrageur closes the gap in a single atomic transaction — buy cheap, sell expensive, both legs execute together. AMMs make this common because they reprice lazily, they only update when someone trades against them. That stale price is the arbitrageur's profit, but it's also what keeps the AMM honest for every user who trades there next.

Over the past 30 days, sandwiched.me tracked over 2.1 million atomic arbs across 248 bot programs. Spikes coincide with major token launches — WIF, Pengu, and the Trump/Melania tokens all generated massive opportunities as price dislocations opened up across venues.

2. Liquidations

Lending protocols let users borrow against collateral. If the value of that collateral falls below a required threshold, the loan becomes undercollateralised, the protocol is holding risk it wasn't designed to hold. Liquidation bots close those positions by repaying the debt and claiming the collateral plus a reward.

Without these bots racing to close underwater positions the moment they become eligible, bad debt accumulates inside lending protocols. Eventually that threatens the solvency of the whole system and puts depositors at risk. Liquidations are the maintenance mechanism that keeps on-chain lending functional, which is why they're consistently classified as good MEV.

3. Back-running

A searcher spots a large trade that just executed and immediately trades afterward to capture the price imbalance it created. The original user doesn't get a worse price because of the back-runner, the opportunity existed because their trade was poorly routed or too large for the available liquidity. It's essentially arbitrage triggered by someone else's trade.

4. Front-running

This is where things get toxic. A searcher sees a pending transaction that will move a token's price and places their own identical trade before it, profiting from the price impact the victim's transaction creates. On Solana, traditional front-running is harder than on Ethereum because there's no public mempool, but it still happens through private mempools and validator-level access to transaction flow.

5. Sandwich Attacks

The most harmful form of MEV. A searcher wraps a victim's trade with two of their own, a buy before and a sell after. The front-run pushes the price to the worst level the victim's slippage will tolerate, the victim's trade executes at that price, and the attacker immediately sells at the inflated level. The victim always fills at maximum slippage. There is no version of this where the user benefits.

Memecoin traders are the most exposed. They set high slippage tolerances on volatile, illiquid tokens just to get trades through, which hands attackers a wide margin to exploit.

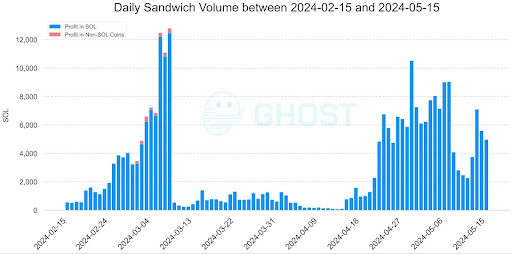

On Solana, sandwich attacks come in two forms. Tight sandwiches bundle the attacker's transactions directly around the victim's in a single atomic package. Wide sandwiches are more aggressive, the bot sends its front-run and back-run hundreds of milliseconds apart instead of bundling them, catching multiple victims in between rather than just one. Over the past 30 days, wide sandwiches alone extracted 77,190 SOL across 759K+ attacks.

Given how much value these attacks extract, the natural question is whether they can be stopped entirely.

Can MEV be eliminated?

The honest answer: no.

As long as someone decides transaction order, that power can be monetized. You can reshape who captures it, but the opportunity just moves.

The Jito mempool closure proved this. When Jito shut its public mempool in March 2024, sandwich activity dropped to near zero overnight. Within 30 days, private mempools replaced it and volume recovered. Jito tried detecting sandwich bundles, bots made them harder to identify. The Solana Foundation blacklisted validators, they spun up new ones. Every door that closed opened another.

The question was never whether MEV could be eliminated — it's who should capture it. Today, most value flows to validators and infrastructure operators. The ecosystem is pushing to shift that toward users and applications whose order flow creates the value in the first place. How that's being built is what we'll cover in Part 2.