Are Solana Validators Profitable?

Every block Solana produces starts with a validator: processing transactions, casting votes, and appending to the chain. That's the work that keeps the network in consensus, epoch after epoch.

It's not lightweight work. Validators run specialized high-performance hardware, maintain near-constant uptime, and vote on every single block the network produces. In return, they earn rewards, a share of inflation, transaction fees, and MEV.

But those rewards are far from equal.

Leader slots, the turns where a validator actually produces blocks and collects fees, are assigned in direct proportion to stake. The more SOL staked with a validator, the more often it leads, the more it earns. Voting influence works the same way. The result is a system where everyone pays roughly the same to operate, but revenue is entirely determined by how much stake you hold.

In this piece, we break down:

- What it actually costs to run a Solana validator

- Where the revenue comes from, and how fragile that mix is

- Who's profitable, who's not, and where the line sits

- Why 75% of validators share just 16% of stake

- How this compares to concentration across other PoS chains

- What Alpenglow, SIMD-228, and other proposals aim to change

- Whether any of it is enough

——————————————

So let's start with the bill.

#1 What it costs to keep a validator running

Solana's validator costs have a specific shape: fixed, unforgiving, and completely indifferent to how much stake you have.

1. Hardware (Fixed Cost)

Solana is one of the most hardware-demanding chains to validate, the specs required sit well above most other L1s.

Running a Solana validator requires bare-metal, dedicated hardware, not a cloud VM or shared server. The network's continuous high throughput demands a high clock speed CPU, large memory capacity, and multiple fast storage drives configured correctly to avoid performance bottlenecks.

As a result, most operators don't buy servers outright, they rent them from professional data center providers. The market consolidation: in Epoch 936, TeraSwitch Networks alone hosted roughly 34% of total staked SOL, followed by Cherry Servers (~8.7%), Latitude.sh (~5.7%), Allnodes (~5.5%), and OVH (~4.4%).

All in, hardware and hosting typically cost $4,000–$8,000/year, depending on provider and region.

2. Data Bandwidth cost

Solana's gossip layer, block propagation, and repair protocols generate constant heavy traffic in both directions. A validator needs at minimum a 1Gbps symmetric commercial line to stay healthy, and most serious operators run on 10Gbps uplinks to avoid falling behind during peak network activity.

2. Operations

Onchain Voting cost: Solana runs consensus voting entirely on-chain, meaning every validator must submit a vote transaction for every block they agree with, directly on the Solana network. Unlike other blockchains where validator signaling happens off-chain for free, every single vote on Solana costs real SOL.

That adds up to roughly 1.1 SOL per day, or ~400 SOL per year, shifts dramatically with SOL's price:

- At $84 (March 2026): ~$33,600/year

- At $150: ~$60,000/year

- At $200: ~$80,000/year

This is what makes voting costs the single most punishing line item in a validator's budget. It's a fixed bill that arrives daily regardless of how much stake you have, how many blocks you produced, or whether you earned anything that epoch.

And critically, there's no way to opt out. The less you vote, the less you earn, and if you stop entirely, rewards drop to zero. But keep voting and you bleed SOL every day. At higher SOL prices, the pressure on undercapitalized validators becomes severe.

#2 Where the money comes from

Validators earn from three sources: inflation rewards, transaction fees, and MEV.

1. Inflation Rewards

Solana mints new SOL every epoch and distributes it to validators and stakers. This is the dominant revenue stream, and for most of Solana's history, it was the only one.

- From February 2021 through mid-2023, validator revenue was nearly 100% inflation, pure green, no fees, no MEV

- Even after fee and MEV income emerged in late 2023 and briefly surged in late 2024, inflation snapped back to ~90-95%+ of total revenue by early 2025

Solana's inflation follows a predefined schedule governed by three parameters:

- Initial Inflation Rate: 8% - the starting rate when inflation was first enabled

- Dis-inflation Rate: −15% - the annualized rate at which inflation decreases each year

- Long-term Inflation Rate: 1.5% - the stable terminal rate the protocol converges toward

The token issuance rate can only decrease from the initial amount. It's already baked into the protocol since launch. The current annual inflation rate sits at approximately ~4%.

Inflation has declined in absolute terms across all validators since February 2021:

- Started around ~200,000 SOL per epoch in early 2021

- Gradually fallen to roughly ~100,000–130,000 SOL per epoch by late 2025

- The curve is smooth and predictable, exactly what a fixed dis-inflation schedule produces

How inflation rewards are generated

Validators participating in consensus receive rewards in SOL, paid via inflation. These newly minted tokens are issued to validators at the end of each epoch. The size of a validator's reward depends on several factors:

- Stake weight: a validator's probability of being selected as block leader is directly proportional to its stake relative to total SOL staked on the network

- Vote participation: validator uptime and the percentage of slots in which it successfully voted affect overall earnings

- Global inflation rate: determined by Solana's pre-set schedule each epoch

What a validator actually keeps from these rewards depends on their commission rate, the percentage they retain before passing the remainder to delegators. In practice, the largest validators have converged on 0%, a rate only viable because their leader slot volume and fee income independently covers operations. For smaller validators, 0% means working at a loss, but charging more means losing delegators to whoever offers better APY.

2. Transaction Fees

Validators receive 50% of the base fee (5,000 lamports per signature) when serving as block leader.

After SIMD-0096:

- 100% of priority fees go directly to the block-producing validator (the leader for that slot)

- 50% of base fees are burned

This was a significant change: before SIMD-0096, validators didn't keep priority fees. Now, the validator who produces a block captures all the priority fee revenue from every transaction in that block.

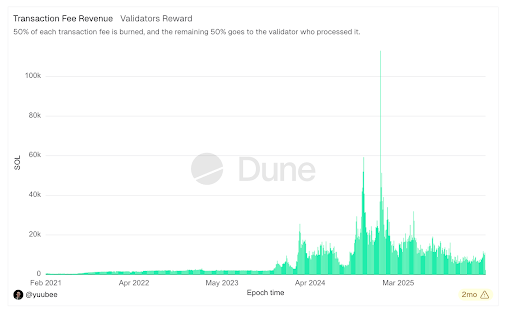

- 2021 through mid-2023: Fee revenue was negligible, nearly flat across the entire period

- Late 2023: Fees started emerging as on-chain activity picked up for the first time

- Late 2024 & early 2025: As on-chain activity surged, fee revenue spiked dramatically. Some epochs saw fees approach or exceed 100,000 SOL, briefly rivaling inflation as a revenue source for the first time in Solana's history.

- Mid and late 2025: Pulled back, but remained elevated compared to anything pre-2024

There's a catch: fee revenue flows through leader slots, and leader slots are assigned proportional to stake. The validators earning the most from fees are the ones who already have the most stake. The fee stream that's supposed to diversify revenue beyond inflation is actually more concentrated than inflation itself.

SIMD-0123 took this further by enabling validators to share block rewards directly with stakers. It's not technically required, but competitive pressure pushes validators towards it:

- If competing validators share block rewards and you don't, delegators move their stake to whoever offers better returns

- Large validators with millions of SOL staked can afford to share and still profit comfortably

- Smaller validators with a few hundred thousand SOL face another squeeze, share what little fee income you earn, or lose stake to someone who will

3. MEV Rewards

MEV (Maximal Extractable Value) is the revenue that revenue validators earn when traders pay extra to prioritize their transactions for arbitrage, liquidations, and front-running opportunities.

The MEV Reward chart tells the clearest boom-and-bust story in Solana's validator economics:

- Zero until mid-2023

- Grew steadily through late 2023 and 2024

- Exploded peaking at over ~110K SOL per epoch around late 2024/early 2025

- Then crashed, falling back to a fraction of its peak within weeks

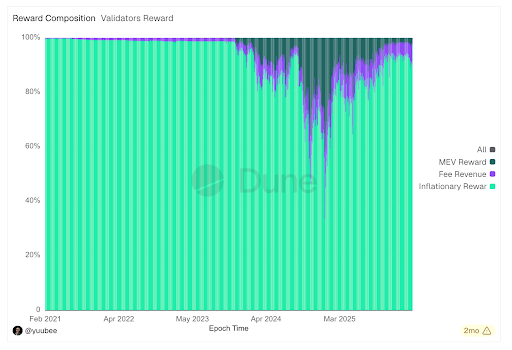

During the late 2024 peak, MEV and fees combined pushed inflation's share down to as low as below 40% of total revenue. For a brief window, it looked like Solana's validator economy had diversified beyond inflation dependence. It hadn't. As activity cooled, the composition snapped back to ~95%+ inflation by early 2025, exactly where it started.

MEV capture depends heavily on infrastructure:

- Jito integration and relay setup

- Which specific transactions happen to land in your leader slots

- Not purely proportional to stake weight, a well-positioned smaller validator can occasionally outperform a larger one

No validator can build a business model around MEV, it arrives unpredictably and vanishes just as fast. Four years of data in one visual:

- 2021 through mid-2023: Nearly 100% inflation. Pure green. Every validator's income was determined entirely by their stake and the inflation schedule.

- Late 2023 – 2024: Fee revenue (purple) and MEV (dark) started appearing, gradually eating into inflation's share.

- Late 2024 – early 2025: The peak. Inflation dropped to as low as ~40% of total revenue. Fees and MEV combined accounted for the majority.

- After early 2025: It snapped back. Inflation returned to ~95%+. The diversification lasted roughly one quarter.

#3 Who's actually making money?

Costs are roughly the same for everyone. Revenue overwhelmingly comes from inflation. So the question becomes: at what stake level does the math actually work?

The economics of scale

The core problem is that costs are fixed but revenue scales with stake.

Every validator pays the same ~1.1 SOL/day in voting costs, the same hardware bills, and the same bandwidth. But inflation rewards, fee income, and MEV all scale proportionally with stake and fees, and MEV compounds further because leader slots are stake-weighted.

This creates a profitability curve that isn't linear, it's exponential at the top and punishing at the bottom.

Validators staking millions of SOL (the top ~19 by stake) earn thousands of SOL per epoch. Their costs are a rounding error relative to revenue. They can charge 0% commission and still profit comfortably, because leader slot volume alone generates enough fee and MEV income to cover operations. For many of them, the validator isn't even the primary business. It supports an exchange, an infrastructure service, or a protocol that makes money elsewhere.

Validators staking 1–2M SOL earn moderate inflation but get infrequent leader slots. Costs eat a meaningful share of their revenue. They're trapped in a commission dilemma:

- Charge 0% commission and bleed money, because inflation rewards all go to delegators and fee income isn't enough to cover costs

- Charge 5%+ and lose delegators to the larger validators offering 0% with better total APY

There's no comfortable middle ground.

Validators staking ~100K SOL are in the most difficult position. According to Everstake's 2025 annual report, the break-even threshold for a validator running 0% commission rose from roughly 24,000 SOL in January 2025 to about 117,000 SOL by October 2025 — a nearly 5x increase in less than a year, driven by declining priority fees and tipping revenue. Even at 5% commission, the break-even nearly tripled from ~20,000 SOL to 62,000 SOL over the same period.

Where the line sits

From the validators.app data (March 2026, 791 validators with non-zero stake):

- Top 19 validators (2.4% of the set) control 33% of stake: comfortably profitable

- Top 50 (6%) control 54%: generally stable

- Top 100 (12%) control 72%: increasingly tight margins

- Bottom ~600 (75%) share just 16%: majority unprofitable or subsidy-dependent

So if the bottom 75% are unprofitable or barely surviving, why are they still running? If 75% of validators share just 16% of stake and voting costs can exceed revenue for the smallest operators, why do they keep their servers on?

Solana Foundation Delegation Program (SFDP)

Most of them aren't running a business. They're running on subsidies, conviction, and bets that haven't paid off yet.

The Solana Foundation Delegation Program (SFDP) was designed to bootstrap new validators by giving them enough stake to cover costs while they built up an external delegation. At peak, 72% of all validators were on the program. The Foundation would delegate a base amount of roughly 40,000 SOL per participant (approximately the amount needed to break even), and match external stake at a 1:1 ratio up to a 100,000 SOL cap.

It worked at getting validators online. It failed at making them self-sufficient.

The numbers tell the story:

- 73% of SFDP validators attracted less than 10,000 SOL from anyone besides the Foundation

- 51% attracted less than 1,000 SOL

- Only 48% were profitable even with the subsidy

- Without it, only 32% survive

The Foundation also covers voting costs for new validators, but on a taper:

- 100% coverage for the first ~3 months

- Steps down to 75%, then 50%, then 25%

- Drops to zero after roughly 12 months

After that first year, the full ~1.1 SOL/day voting bill lands on the validator. For operators who never attracted meaningful external stake, that cliff is often fatal.

The Foundation has since tightened the program significantly. The delegation pool was cut from 100M to 51M SOL. Their share of total network stake dropped from 44% to under 6%. They introduced the "onboard 1, offboard 3" rule: for every new validator added, three that have been on the program 18+ months without attracting even 1,000 SOL independently get removed. The Foundation president called these operators "VINO", Validators In Name Only.

The foundation also stopped giving inflation awards to malicious validators using Jito product back in the day, which allowed for sandwiching and private orderflow.

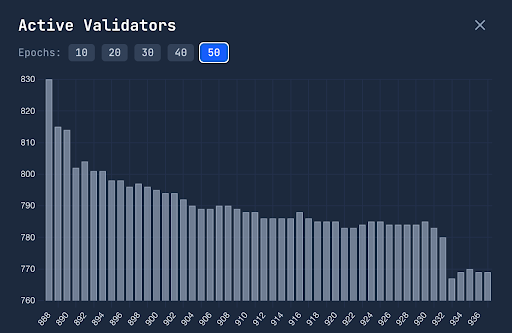

The result: Solana's active validator count dropped from roughly 1,500 to 2,000 down to ~800. Most who left were small no-stake nodes that existed primarily because of SFDP.

#4 Solana Validators Profitability

The Solana Validators Profitability dashboard confirms what the economics predict.

Using a 10-epoch average (epochs 926 to 935, $20,000/year infrastructure, SOL at $84.99), out of 792 validators tracked:

- Profitable: 494

- Break-even: 118

- Unprofitable: 180

Roughly 1 in 4 validators is losing money over a sustained 10-epoch period. Another 1 in 7 is barely breaking even.

Single-epoch snapshot (epoch 935), all 770 validators:

- Profitable: 462 (60%)

- Break-even: 102 (13%)

- Unprofitable: 206 (27%)

The picture gets worse when you isolate validators dependent on Foundation support.

SFDP validators only (epoch 935), 440 validators:

- Profitable: 226 (51%)

- Break-even: 83 (19%)

- Unprofitable: 131 (30%)

Nearly half of all subsidized validators are either breaking even or losing money, with the subsidy included. The program designed to make them viable hasn't.

SFDP validators also receiving vote compensation (epoch 935), 146 validators:

Vote compensation is the maximum level of Foundation support. On top of receiving delegated stake, the Foundation covers some or all of the validator's ~1.1 SOL/day voting expense. If you can't be profitable with free stake and free voting, the economics fundamentally don't work.

- Profitable: 69 (47%)

- Break-even: 36 (25%)

- Unprofitable: 41 (28%)

More than half aren't turning a profit. Even with both forms of support.

These ratios have been remarkably stable across the 10-epoch window. The profitable, break-even, and unprofitable lines barely move from epoch to epoch. This isn't a temporary dip caused by a bad market or a slow week on-chain. It's the steady state of Solana's validator economy.

The flywheel that makes it worse

The concentration compounds through a self-reinforcing cycle:

- More stake → more leader slots

- More leader slots → more fee and MEV income

- More income → ability to charge lower commission

- Lower commission → attracts more delegators

- More delegators → more stake

Nothing in the current protocol interrupts this loop. The validators who are profitable become more profitable. The ones who aren't fall further behind. Every epoch, the gap widens.

Effective concentration is also higher than the raw validator count suggests:

- Coinbase runs 5+ validators (Coinbase, Coinbase 02, 03, 04, 05)

- SOL Strategies runs 4+ (Laine, Cogent, Orangefin, SOL Strategies)

- Figment appears at least twice (Figment, Ledger by Figment)

- RockawayX runs 3 (RockawayX Infra, RockawayX Firedancer, Solmate)

- P2P.org runs 3 (P2P.org, P2P.org Turbo, P2P.org Labs)

Consolidate by entity rather than validator address, and the top 10 organizations likely control 40%+ of all stake.

#5 Stake Concentration is a Proof-of-Stake Problem

Researchers measured validator stake distributions across ten major PoS blockchains — Aptos, Axelar, Binance, Celestia, Celo, Cosmos, Injective, Osmosis, Polygon, and Sui. Regardless of chain or consensus design, every single one showed the same result: a small group of validators controlling a disproportionate share of power.

Why this happens: the flywheel

In any stake-weighted system, the rules are simple:

- More stake → more block proposals → more revenue

- More revenue → lower commissions → more delegators attracted

- More delegators → more stake → repeat

Every epoch, this flywheel spins. On Solana, where validator rewards scale directly with delegated stake and leader slots are assigned proportionally, the same dynamic plays out.

Rich get richer, even when everything is fair

The Ethereum Foundation ran simulations tracking how validator balances evolve over time. They gave all validators identical income — same rate, no randomness. Inequality still grew.

A larger validator accumulates more in absolute terms each epoch. They activate new validators sooner. Those validators generate more rewards. The gap widens automatically, with no one doing anything wrong, purely as a consequence of starting from different positions.

#6 What changes when voting goes offchain with Alpenglow

Solana's current consensus runs on Tower BFT, where validators vote on every block by posting onchain transactions, and those votes lock in over time through exponential lockout periods to prevent reversals.

This design works, but it comes at a cost. Onchain voting is the single largest validator expense — ~1.1 SOL/day, identical for everyone regardless of stake.

Alpenglow's new Votor component shifts validator voting off-chain, eliminating the fixed per-vote transaction costs that currently make running a smaller validator economically unviable.

No more per-slot voting fee. No more blockspace consumed by vote transactions.

The VAT replaces voting costs

Moving votes off-chain eliminates voting fees, but it creates a Sybil problem: without a cost to participate, large stakers could spin up fake validators to crowd out smaller ones. So Alpenglow introduces the Validator Admission Ticket (VAT): a flat fee to participate in consensus.

- Current voting cost: ~1.1 SOL/day

- Alpenglow VAT: ~0.8 SOL/day — a ~20% reduction

- The entire VAT gets burned, directly reducing token supply

A 20% savings is meaningful but not transformative.

#7 Where does this leave us?

Stake pools are one of the few levers that can shift distribution without waiting for a protocol upgrade or a governance vote. As we covered in our previous articles on liquid staking and LSTs, the infrastructure already exists. When a user stakes through a well-designed pool, their SOL gets spread across hundreds of validators using a delegation formula that actively routes stake toward validators that would otherwise struggle to attract delegation on their own.

Some pools score validators on performance, commission, and decentralization metrics. Others introduce bonding mechanisms that create validator accountability without any protocol-level enforcement. These are real, working tools.

But they have a ceiling. Stake pools optimize for their users' returns first, decentralization second. A pool that favors smaller validators at the cost of APY loses deposits to competitors who don't. The mechanism works — the question is whether enough stake actually flows through pools designed this way to move the needle at the network level.

Right now, it doesn't. The flywheel keeps spinning regardless. Stake pools are a meaningful piece of the puzzle. They are not, on their own, the answer.